Adopting contactless payments in US public transit: overcoming the challenges

Contactless payments are transforming public transit in the US one

Transit ticketing and fare collection has evolved through 3 major phases over the decades;

Cash, Closed Loop and Open Loop. Cash fareboxes were introduced in the 1880s, followed by token-based systems in the 1930’s which reduced the need for cash handling. In the 1990s, magnetic stripe cards, like New York’s MetroCard emerged enabling stored value and convenient swiping at fare gates, marking a shift towards smartcard based systems.

Closed Loop systems (Smartcards)

A closed loop payment card is a type of card that can only be used at a specific set of merchants or locations, rather than being accepted widely like a credit or debit card. These cards are typically issued by a specific organisation, and can only be used to make purchases within that organisation’s network of products or services.

An example is a transit card, which is used for transportation systems such as buses, subways, and trains, and can only be used within the transit system’s network. There are many examples of these around the world such as: Oyster Card (London), Myki (Melbourne), Clipper (San Francisco), Leap Card (Dublin). The Octopus card in HongKong is a somewhat unique example of a transit closed-loop card that was then opened up for use by other retailers.

Closed Loop cards are sometimes referred to as Smartcards, or Stored Value Cards. The card itself usually holds data about the amount of funds currently held by the customer, and is adjusted through a back-office, or ledger system for the application.

The value on the card can be ‘topped up’ by the customer by cash (at a Kiosk or Retail outlet) or through an online payment using an Open Loop card.

Open Loop Systems (Bank issued cards)

Open loop payments are typically associated with payment cards such as credit cards, debit cards, and prepaid cards. These cards are usually issued by financial institutions such as banks.

Open loop payments are processed via payment card networks (also referred to as “schemes”) that facilitate the transfer of funds between the merchant’s bank and the customer’s bank, and provide security and fraud prevention measures to prevent loss.

These systems (sometimes referred to as ‘payment rails’) have been developed over several decades and billions of dollars of investment. Visa and Mastercard are the two largest open card networks.

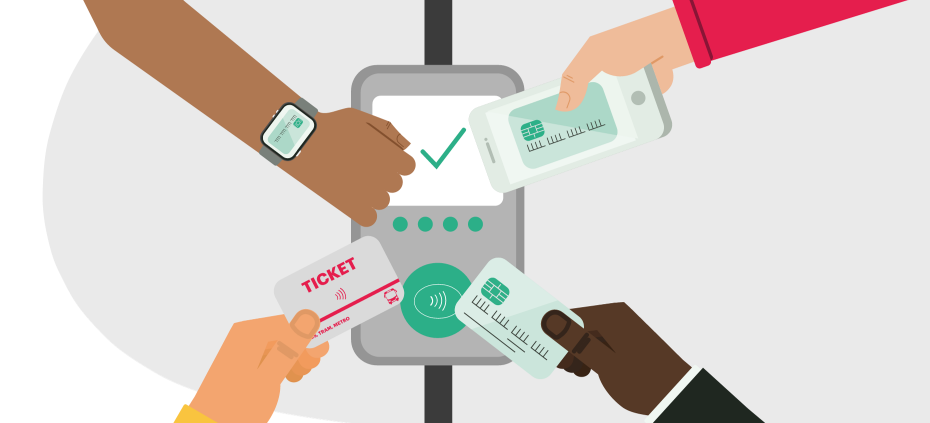

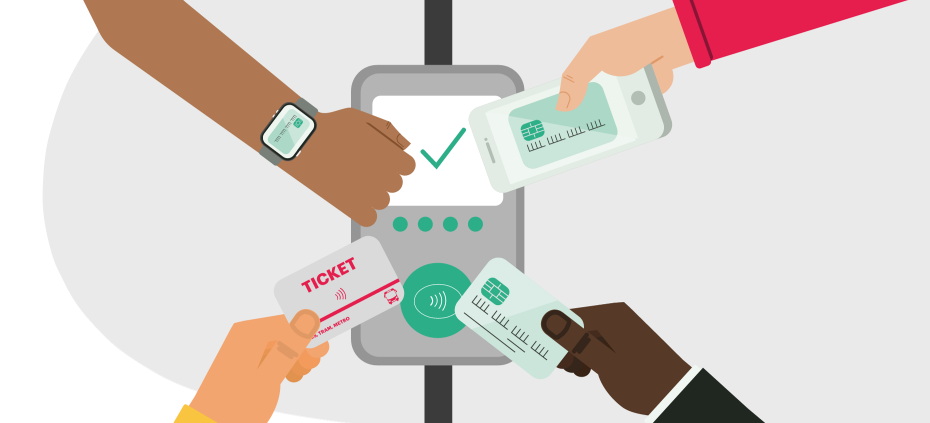

When we refer to ‘contactless payments’ in transit, we are usually referring to a particular type of Open Loop payment – that doesn’t require card insertion or a swipe.

In 2007, the UK card industry set contactless payments in motion to provide a fast and frictionless payment experience in retail. Shoppers could now buy their groceries, the weekly newspaper or a pair of socks all with a simple tap of their card at the checkout.

Today, contactless accounts for 50% of global in-person transactions handled by Mastercard1, and the global contactless payment market is projected to garner $32.75bn by the end of 20242.

The speed at which customers could just tap and pay proved ideal in fast-moving………..

To continue reading the article, please complete the form below:

NOTES:

Contactless payments are transforming public transit in the US one

Sustainability, mobility and equity have become touchstones of modern public

Successful apps have one thing in common. They just work.

America’s public transportation systems face existential challenges. Ridership hasn’t yet